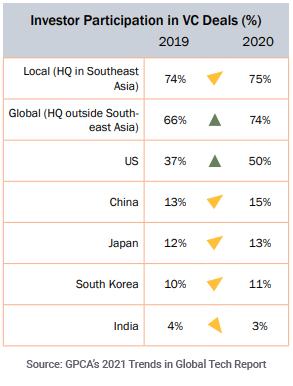

How has the VC ecosystem in Southeast Asia evolved for early-stage investors since Openspace Ventures was founded in 2014? Is the ecosystem at an inflection point, with the Gojek/Tokopedia merger and upcoming Grab SPAC?

This is undoubtedly an exciting time for the venture ecosystem in Southeast Asia. There was the first wave of billion-dollar internet giants in the region, like Grab, Sea and GoJek, which has had a magnetic effect in terms of attracting global interest. Second, after a patient, decade-long journey, the path to meaningful liquidity for companies is clearer than ever before, with public markets opening up and the increasing presence of SPACs in the region. Third, while there will always be too much capital chasing too few good deals in venture, there is ever more competition in the region, with Chinese and US investors, even those without specific regional coverage, doing an increasing number of deals on an ad-hoc basis. Finally, several firms within the ecosystem are becoming multi-stage, with venture capital raising growth funds and private equity willing to do earlier-stage deals.

Openspace Ventures held a USD120m first close this year for its first growth fund, with a USD200m target. What strategy, sectors and ticket size will this fund target?

The launch of Openspace’s growth fund, OSV+, reflects the extent to which the Southeast Asia market continues to evolve and mature. This fund will focus on mid-stage growth opportunities, largely Series C and D rounds, and will enable us to continue doubling down on companies we previously backed at Series A and B stages. At the same time, it opens up opportunities to invest in an increasing set of other companies operating at a similar stage. At this point, there are only a few funds focused exclusively on this stage. Our strategy remains the same as our early-stage funds in that we will focus on Southeast Asia tech with a sector-agnostic approach. We actively seek to back the companies and founders in the region creating a transformative impact.

Openspace invests across a range of sectors. What are the particular sectors you are focused on right now and what is the opportunity you see there? Can you share any examples of investments you have made in these sectors?

Our thesis from the outset was that the region’s startup ecosystem would be largely fueled by companies addressing fundamental tertiary needs. Amongst others, these included health, finance, agriculture and education. Even back in 2014, we recognized the impending demand for a widescale digital infrastructure and invested in superapp Gojek at the Series A, when it was still just a motorbike ride-sharing solution. The market conditions in Indonesia ensure it continues to receive a disproportionate level of investor interest. As a result, rather than diversifying at the sector level, we are now making high conviction investments in a broader set of markets, notably Thailand and the Philippines. We believe both are at exciting inflection points and are beginning to represent exceedingly good value for money. The impressive growth demonstrated by our portfolio company Kumu, a live-streaming platform connecting the Filipino diaspora, is clear evidence of this new traction, having registered 1000% revenue growth year over year. Equally, we just led the Series A round for SCB Abacus, an alternative digital lending platform in Thailand, with their loans disbursed increasing by 10x in the past year alone.

This year, Openspace led a USD20m pre-Series B for Pluang (Indonesia – wealthtech) and invested in Nano Technologies (Vietnam – payroll advances). How do you look at the fintech opportunity in Southeast Asia? What gaps are these startups filling in the market?

We recognized at an early point that fintech would be one of the most significant opportunities in Southeast Asia. Whenever we assess a market opportunity, we start by asking, “Why now?,” and why the market change would matter to people. In the case of fintech, we observed a coming together of high smartphone adoption, large unbanked populations (estimated to be around 73% even in 2021) and people with limited access to credit. Our belief was that by unlocking credit and growing individual wealth, the latent potential of the region would be unleashed, improving financial inclusion and quality of life for the region’s population.

For that reason, we have invested in startups like Nano as a unique way of extending credit in Vietnam. The market continues to grow as people seek greater financial education and more diverse investment opportunities. For example, our portfolio company Pluang, which expanded into asset classes including single stocks and cryptocurrencies, has seen impressive uptake across a broader base of users.

With more Southeast Asian companies going public and the increasing presence of SPACs in the region, how is the exit landscape changing for venture-backed startups in Southeast Asia?

With companies like Sea, Grab and GoTo (Gojek) leading the way, the US IPO exit path has been firmly established. We will see others follow in their footsteps, with PropertyGuru having been reported as exploring a SPAC listing. However, recent listings such as Bukalapak on the IDX might be the initial signals of a broader paradigm shift. It is expected that other homegrown Indonesian brands, such as Traveloka and Tokopedia, could be tempted to list in their home country too, as national governments look to make listing on local stock exchanges more attractive for big tech companies through regulatory changes. The Thai and Singaporean stock exchanges should not be overlooked in the exit consideration set. It’s not unreasonable to think that they will catch up soon. In addition, the overall exit landscape and path to liquidity is looking healthier as the Southeast Asian ecosystem matures, with M&A activity being increasingly driven by local tech giants in addition to the established international buyers.

Are ESG considerations part of Openspace’s investment decision-making process? Please provide examples from the portfolio of how you are implementing ESG practices and/or tracking KPIs related to environmental impact, social inclusion, access to education, healthcare and affordable credit.

At Openspace, ESG considerations are an integral part of our pre- and post-investment processes. We review and score investments with reference to international standards including the IFC Performance Standards and work closely with portfolio companies to implement ESG best practices, either by directly providing resources, hosting capacity-building workshops or making introductions to consultants. As a fund with investments spanning a wide range of industries, we develop and track appropriate impact metrics with specific portfolio companies such as accessibility (of health, credit, education) to underserved groups, and on the portfolio level, we monitor overarching indicators including job creation and gender diversity. We apply these concerns to our own firm and have led the way by publishing our own Sustainability Report in 2021 and are proud to have 50% female representation across the firm – including at the most senior levels.