Data Highlights from EMPEA’s 1H 2014 Industry Statistics

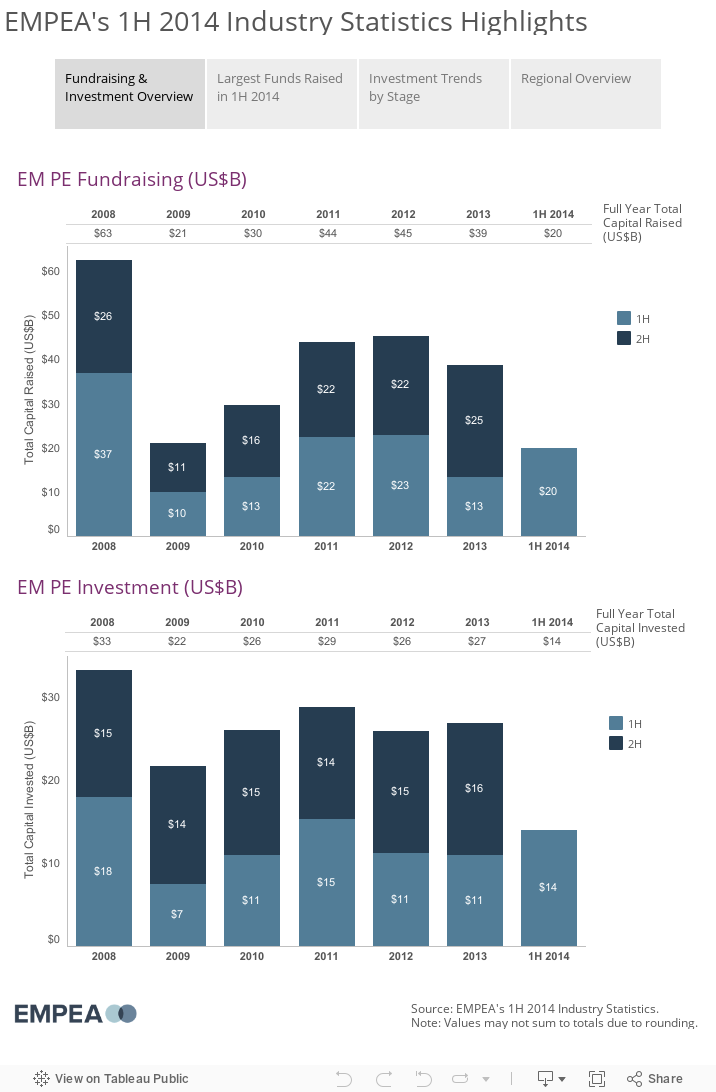

According to EMPEA’s 1H 2014 industry statistics released last week, private equity (“PE”) fundraising and investment activity for emerging markets (“EM”) were off to a strong start in the first half of 2014. Fund managers raised US$20 billion and invested US$14 billion in 1H 2014, corresponding to a 48% and 28% increase, respectively, compared with the same period in 2013, and on pace to surpass last year’s totals.

Notable EM PE trends from the first half of 2014:

- A number of well-established fund managers successfully returned to market and closed large vehicles—Capital raised for EM PE vehicles increased 48% in 1H 2014 compared with 1H 2013; yet, only four more funds held a close in the first half of the year compared with the same period last year, suggesting a continued concentration of capital in fewer funds. The three largest EM PE funds to hold a close in 1H 2014, Affinity Asia Pacific Fund IV, CVC Capital Partners Asia Pacific IV and TPG Asia VI, all with pan-Asia remits, together accounted for US$5.1 billion, or 26%, of the first-half capital raised for emerging markets.

- A rise in venture capital and buyout fundraising and investment activity suggests that investors increasingly look to access opportunities in emerging markets via multiple strategies—Buyout vehicles and venture capital (“VC”) vehicles accounted for 37% and 27% of funds raised, respectively, in the first half of 2014. Funds raised by buyout-focused vehicles in 1H 2014 represented the highest proportion of total capital raised since 2008, and the surge in VC fundraising led the strategy to surpass growth capital vehicles for the first time since EMPEA began tracking statistics in 2006. China and India dominated VC fundraising and investment activity in 1H 2014. Of the 28 emerging markets VC funds to hold a close in the first-half, 19 had a geographic focus on China or India, and the two markets together accounted for 70% of all EM VC deals.

- Emerging Asia continued to dominate activity, but Sub-Saharan Africa gained the most ground— Emerging Asia fundraising and investment in the first half of 2014 accounted for 76% and 78% of overall EM PE, respectively. In comparison, Sub-Saharan Africa gained the most ground, comprising 11% of total capital raised for emerging markets, the highest proportion on record. Sub-Saharan Africa-focused vehicles raised US$2.2 billion in 1H 2014 and surpassed annual totals for the region since 2008. Fundraising was driven by four vehicles raised by The Carlyle Group, Amethis Finance, Helios Investment Partners and Investec Asset Management, which represented 75% of the total capital raised for the region.

See below for data highlights behind these trends.

Select the grey headline to view the associated chart. Selecting any item from a chart’s legend isolates it within the dashboard view.